New Bretton Woods: Part 9. The bill

Or: the cap table, read out loud

Part 8 ended with a photograph and a promise. The photograph was the Brussels dinner of 2017: eight people, a populist vehicle, a Belgian lawyer, a 501(c)(4) structured for opacity by Jeffrey Epstein, and at the far end of the table a gold miner with Chinese-state joint ventures whose presence nobody had been able to explain. The promise was that the retailers would step aside and the invoices would be read out. This part keeps it. Everything the previous eight parts described as motion, doctrine travelling, money moving, personnel circulating, resolves here into a single static object: a list of who holds what, and what each position pays out under which condition. The series has been an argument that modern politics, read accurately, is the marketing department of a trade. This part is the trade itself, with the marketing stripped off.

It needs three things stated before the figures, because without them the figures read as a conspiracy theory, which is the one thing this series has spent eight parts refusing to be.

Three frames, restated

The first is that almost no one named in this series is breaking the law as currently written. That is not a weakness of the argument. It is the argument. The legal architecture of the United Kingdom, the United States and the European Union was built for a world in which political influence, financial extraction and foreign interference were three separate offences, pursued by three separate agencies, under three separate statutes. The Electoral Commission polices donations. The Financial Conduct Authority polices markets. The Foreign Influence Registration Scheme polices agents of foreign powers. What has been assembled in front of us is a structure that is none of these things taken singly and all of them taken together: a continuing enterprise that earns in the financial layer, protects its earnings in the political layer, and draws its strategic cover from the foreign-policy layer, with the same people moving between the three. No single regulator can see the whole of it, because no single regulator was built to. The Electoral Commission cannot subpoena a Treasury Secretary. The Financial Conduct Authority cannot read a Lords Register entry against a leaked Mauritius beneficial-ownership file. Each agency sees its own slice, finds it largely compliant, and files. The compliance is real. The slicing is the problem.

The second is that conspiracy is the wrong word, and conspiracy theory is the wrong response. The documentary record does not show a plot. It shows enterprise, in the precise sense the American racketeering statutes give the word: a continuing structure of named individuals in named relationships, producing coordinated outputs without a central command issuing orders. Each operator maximises returns inside his own position. Harborne funds the party whose policy is his asset’s tailwind because that is rational for Harborne. The Trump family issues the stablecoin whose yield is the public’s foregone revenue because that is rational for the Trump family. Musk sells the future that makes extraction feel like progress because that is rational for Musk. The outputs align not because anyone coordinates them but because the positions are positioned in the same trade, and a trade does not need a conductor any more than a shoal needs a choreographer. RICO does not require conspiracy. It requires enterprise, and enterprise is exactly what the cap table documents.

The third is that none of this is hidden. Every figure in this series, every donation, every cap-table line, every offshore beneficial-ownership entry, every dinner and every podium, sits in the public record or in leaked records that mainstream investigative journalism has already authenticated. There is no smoking memo because there was never any need for one. The information operation here is not concealment. It is distribution: the burying of a legible structure under so much volume, vocabulary and plausible deniability that the structure becomes invisible not because it is secret but because it is everywhere. Reading the bill is therefore not an act of revelation. It is an act of addition. The line items have all been published. They have simply never been totalled.

So here is the total.

The single trade

Strip the eight parts to their mechanism and one trade remains, with two legs and a brace.

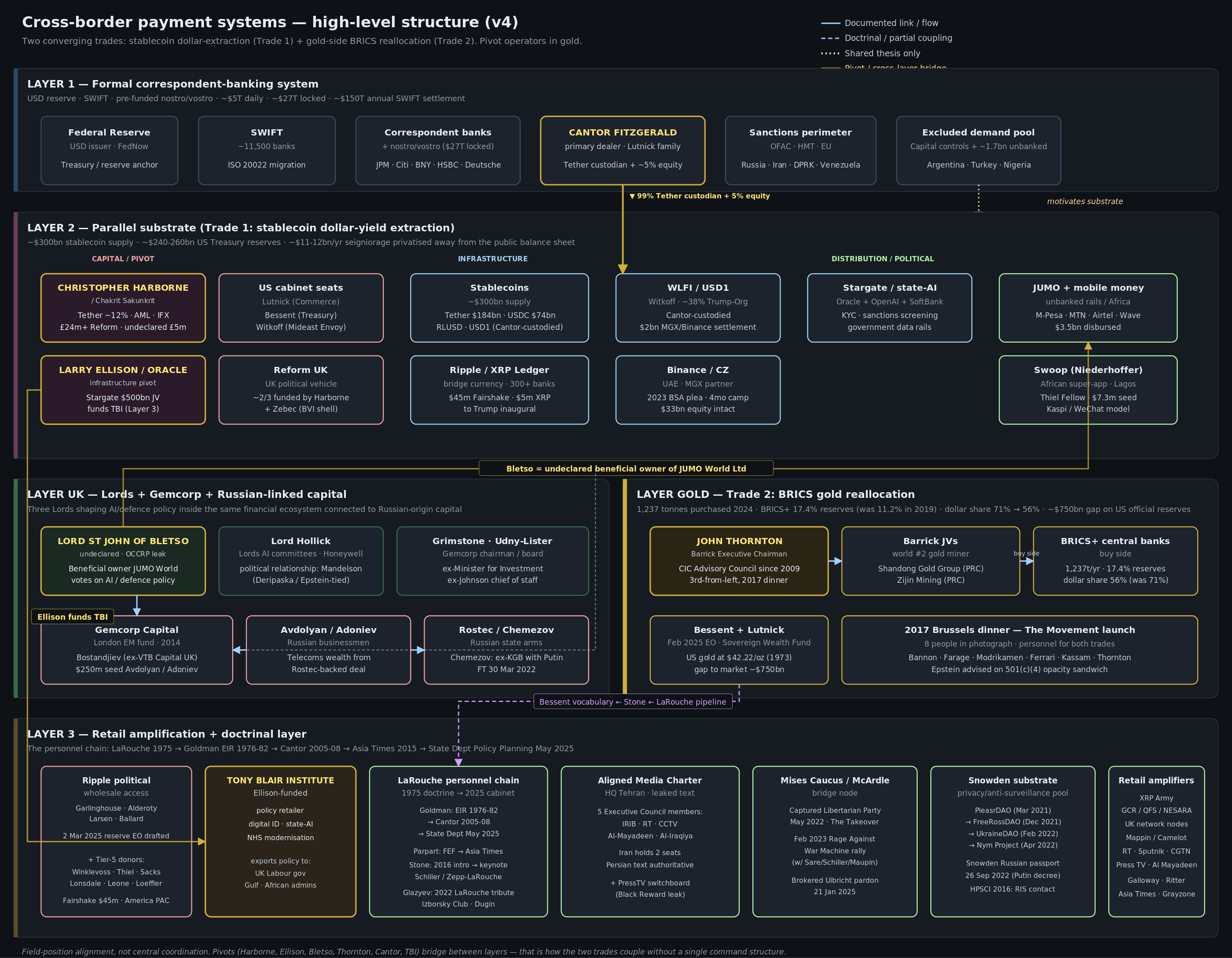

The first leg is the stablecoin float, the subject of Part 3. A stablecoin is a private claim on US Treasury yield wearing the costume of a payment instrument. The issuer takes dollars, holds them in short-duration Treasuries, pays the holder nothing, and keeps the interest. This is no longer an estimate. Tether closed 2025 with around 141 billion dollars of US Treasury exposure, 122 billion of it held directly, against roughly 186 billion dollars of USDT in circulation; the issuer disclosed a net profit for the year of over ten billion dollars, and distributed more than ten billion in dividends across the first three quarters alone. That ten billion is the bill, in a single line. It is the yield on dollars the public created, collected by a private holder and paid out to its owners, and the largest single owner of that holder, with a stake of around twelve per cent, is Christopher Harborne, the man who also funds two-thirds of Reform UK. Across the whole sector, issuers now hold something over 182 billion dollars of US Treasuries collectively, which makes the stablecoin industry, taken as one entity, a larger holder of American government debt than South Korea or the United Arab Emirates. The leg pays on the way down: for as long as the dollar is trusted, every basis point of yield it commands is money the issuers collect and the Treasury forgoes. And the structure is now confirmed in statute, because the GENIUS Act of July 2025, the sector’s own enabling legislation, expressly forbids issuers from passing the yield to the holders. The law does not merely permit the privatisation of seigniorage. It mandates it, by making the one arrangement that would return the yield to the public, an interest-bearing stablecoin, illegal. Cantor Fitzgerald, whose principal is now Commerce Secretary, holds roughly five per cent of Tether through convertible debt and custodies a competing issuer’s reserves besides. The President’s family runs its own issuer, USD1, and books the same yield on a smaller float. None of it is hidden. It is BlackRock-managed, BitGo-custodied, BDO-attested and disclosed in prospectuses. It is simply never totalled, and never named for what it is.

The second leg is gold, the subject of Part 6’s keystone section. Gold is the asset that pays on the way up. If the dollar’s reserve status erodes, and the central banks have voted with more than a thousand tonnes a year of purchases since 2022 that they expect it to, then the metal reprices, and whoever holds the metal, or the miners, or the revaluation option on a sovereign hoard, collects the gain that the dollar-holders lose. The central-bank accumulation is the market’s own forecast, stated in bullion: BRICS-aligned reserves up from roughly eleven per cent of the global total in 2019 to over seventeen per cent now, the dollar’s share down from seventy-one per cent at the century’s turn to around fifty-six, the lowest in three decades. John Thornton is the clearest single embodiment of the position, executive chairman of the world’s second-largest gold miner, joint ventures with two Chinese state miners, a seat on the China Investment Corporation’s advisory council held continuously since 2009, a foot in both the American and the Chinese gold complexes. And the American state itself now holds the largest single revaluation option in existence: the gold reserve carried on the books at the statutory 1973 price of 42.22 dollars an ounce against a market price more than sixty times higher, a latent gain of something like three-quarters of a trillion dollars, which the February 2025 sovereign-wealth-fund executive order exists precisely to monetise, in the Treasury Secretary’s own phrase, by “monetising the asset side of the US balance sheet.” The two legs sit in the same cabinet. The Commerce Secretary’s family bank holds the stablecoin that pays on the way down. The Treasury and Commerce secretaries jointly hold the revaluation option that pays on the way up. A single administration is hedged across both sides of the dollar’s managed decline, and has written the hedge into an executive order.

The brace across the two legs is the physical-asset side, Part 6’s compute-and-resources argument: the data-centre buildout that fences scarcity and prices its admission in a currency whose yield is being privatised, and the rare-earth and uranium positions that collateralise it. The buildout goes where the dollar perimeter is being decoupled, cheap stranded power, weak enforcement, leaderships open to dollar-adjacent infrastructure, and the same equity holders recur across the compute layer, the yield layer and the metal layer because it is the same room, a phrase this series has now earned the right to use literally. The clearest single seat on this side is Larry Ellison. Ellison owns around forty per cent of Oracle, a stake whose value ran past 300 billion dollars in 2025 on the strength of the company’s leadership of Stargate, the 500 billion dollar American compute initiative anchored by an OpenAI contract reported at over 300 billion. He is the physical-asset leg made flesh: the man who fenced the compute, secured priority on the chips, and wired Oracle’s fate to the most strategically important research lab in the world, with the President himself among the announced backers of the initiative. And he sits in the same trade for the same reason as everyone else in this series, because his position behaves the same way: he has pledged about a third of his Oracle shares as collateral against personal debt, which is the Musk pattern from Part 8 exactly, narrative-inflated equity, leveraged, value conjured by a story about the future and borrowed against in the present. When the restructured TikTok US was assembled in early 2026, a fifteen per cent stake went to an Oracle-led group, so the distribution layer joined the compute layer in the same hands. Stargate manufactures the scarcity. TikTok distributes the story that makes the scarcity feel like progress. Both are Ellison’s, and both are the brace.

Around the trade sit the supports the other parts documented. Russia and China supply the geopolitical leverage that accelerates the erosion, Part 7’s settlement rails and Part 6’s gold convoys. The messenger chain from LaRouche through Goldman to Stone to Bessent supplies the doctrinal cover, Parts 2 and 5. The retailers, Reform, the Trump administration, the Musk and Thiel complex, Blair in a suit, supply the political protection, Part 8. And the contaminated vocabulary, the methodology note’s subject, supplies the register in which serious commentary reproduces the trade’s own framing without noticing it is doing so. Eight parts, one object. The object is a privatisation.

What is actually being built

The series has spent eight parts on who profits and who sells. It has said less about the thing itself, the actual machine, and a bill should describe the goods. What is being built is a second cross-border payment system, assembled in parallel to the first and designed to bypass it.

The first system is the one that has run the world since 1944: the correspondent-banking network, dollar-denominated, messaged over SWIFT, settled through pre-funded accounts that banks hold in one another’s currencies abroad. It moves something like five trillion dollars a day. It is slow, taking two to five days for a cross-border payment, it is expensive, layering fees at every tier, and it locks up an estimated 27 trillion dollars globally in the dormant foreign-currency balances that grease it. Crucially, it is also the instrument through which financial measures against states that break international law are enforced, because to be cut off from correspondent dollar banking is to be cut off from the system, which is why the perimeter, the OFAC and Treasury and EU lists, excludes Russia, Iran, North Korea and Venezuela. The same architecture that settles trade also enforces consequence. That dual function is not a flaw the parallel system fixes. It is the feature the parallel system is built to remove.

The parallel system has no central command, which is exactly the point this series has made from Part 1. It is a set of operators occupying adjacent positions around one shared thesis: the formal system has gaps, fill them. At the settlement layer sits Tether, whose USDT is the dominant instrument in the corridors the formal banks will not or cannot serve, the sanctioned-jurisdiction trades, the capital-flight channels, the remittance routes, with Harborne holding his twelve per cent at one end and the unbanked emerging-market user at the other. Alongside it sits Ripple, whose XRP is pitched as a bridge currency to replace the pre-funded accounts entirely, and which paid 45 million dollars into the Fairshake political-action committee in the 2024 cycle, donated five million in XRP to the Trump inaugural, and whose lobbyists drafted the strategic-crypto-reserve announcement the President made on 2 March 2025. At the consumer layer sit the credit and mobile-money rails: JUMO, the banking-as-a-service platform for the unbanked, founded 2015, Mauritius-registered, Goldman Sachs and Gemcorp and Visa among its backers, the same JUMO whose Lords-Register shadow runs through Part 7 and reappears below; the mobile-money operators M-Pesa and MTN and Airtel and Orange that already carry most of the world’s mobile-money users across Africa; and, at the speculative frontier, Swoop, a 2025 venture by a nineteen-year-old Thiel Fellow, seeded in April 2026 with 7.3 million dollars from a16z’s crypto arm and adjacent funds, a food-delivery wedge in Lagos with a stated fintech endgame and an explicit super-app model. The thesis each of them states aloud is the same: in markets with no legacy banking infrastructure, you do not compete with the old rails, you replace them. Stated as financial inclusion, it is unimpeachable. Read against the rest of the trade, it is the construction of a settlement system outside the perimeter that enforces international law, funded by the same capital pool and protected by the same politics. Harborne is the proof that the layers are one structure and not three: through AML Global, his aviation-fuel brokerage, and IFX Payments, his cross-border money business that bridges formal banking and crypto rails, and his Tether stake, and his Reform donations, a single person holds the settlement instrument, the on-and-off ramp, and the political funding at once. The framework does not need him to coordinate the others. It needs only that the position pays, and it does.

Above all of it sits the retail doctrinal layer, the public-facing register that recruits to the substrate: the Global Currency Reset and Quantum Financial System and NESARA mythologies, the claim that a slate of pre-selected coins will be revalued overnight when the old system collapses, pushed by a content economy of mid-tier influencers and expat-libertarian boosters. These claims are not engineering. A coin being “ISO 20022 compliant” means only that its software can read a message format any payment system can read; it is not a prophecy. The mythology is not a description of the machine. It is the recruitment vocabulary for it, the retail end of the same doctrine the wholesale tier sells at Tsargrad and the Schiller Institute, and its function is to keep retail attention rotating toward the next imminent revaluation while the actual positions accumulate underneath. The doctrine sells the dream. The substrate banks the float.

The messenger chain, assembled

The cabinet is where the chain terminates, and it is worth assembling in one place because the employment records do the work that rhetoric is usually asked to do.

David Goldman ran the economic-publications desk of the LaRouche organisation’s Executive Intelligence Review from 1976 to 1982. He passed through Credit Suisse and Bank of America, then became Global Head of Fixed Income Research at Cantor Fitzgerald from 2005 to 2008, which is to say he worked for Howard Lutnick. In 2015 he and Uwe Parpart, the same Parpart who explained the Strategic Defense Initiative on American breakfast television in 1983 for the Fusion Energy Foundation, took over Asia Times and ran the doctrine under a Hong Kong dateline without the LaRouche letterhead. In May 2025 Goldman entered the State Department’s Policy Planning Staff as Senior Advisor. Scott Bessent announced his candidacy for the Treasury on Roger Stone’s WABC radio show in November 2024 and told Stone, on air, that he wanted to be part of “Bretton Woods realignments,” the exact phrase LaRouche had been promoting since 1975. Stone himself was introduced to LaRouche’s senior aide Harley Schlanger in 2016, keynoted a Schiller Institute conference in 2018, and conducted LaRouchePAC interviews into 2020. Lutnick is now Commerce Secretary. The line runs from a 1976 economic-publications desk in Leesburg to two cabinet departments and a State Department planning staff in 2025, and every step of it is in a published employment record or an on-air recording. The vocabulary did not travel by coincidence. It travelled by payroll.

The enforcement gap, in exhibits

Frame one said the operators are mostly not breaking the law. The proof of that is not assertion. It is a small stack of dismissal letters, and they are the most useful documents in the series, because each one shows a different agency finding a different reason to file a different slice of the same structure as compliant.

Take the House of Lords. On 11 December 2025 a set of complaints was filed with the Lords Commissioner for Standards against four peers connected, through the Gemcorp and JUMO chain documented in Part 7, to the same frontier-finance architecture. Five days later, on 16 December, all of them were dismissed. The Bletso complaint, reference 2526-42, concerned a holding in JUMO World and was dismissed on the ground that the shareholding fell below the registrable threshold of a controlling interest. That is defensible on the registration rule and it dodges the merits, because the Lords Code carries a declaration duty, at paragraph 19, that is broader than the registration duty and is not threshold-bound: a peer must declare a relevant interest when participating in relevant proceedings, whatever its size. The dismissal engaged the registration limb, which the threshold defeats, and never engaged the declaration limb, which it does not. The Hollick complaint, 2526-43, was dismissed as time-barred under the four-year rule. The Grimstone and Udny-Lister complaints, 2526-44 and 45, concerning Gemcorp directorships, were dismissed as compliant on the register as it stood. Three different exits, threshold, time bar, facial compliance, each individually sound, each routing around the substance, all delivered inside a single working week. That is not corruption. It is the enforcement gap operating exactly as designed: a complaints architecture built to test isolated entries against isolated rules, confronted with an integrated structure it has no instrument to see whole, finding each fragment in order and the sum invisible.

The same shape recurs at the Commons end, where the Parliamentary Standards Commissioner’s inquiry into the undeclared five-million-pound Harborne gift to Farage, Part 8’s sharp object, will turn on a declaration question, not an enterprise question, because declaration is the only question the Commissioner is empowered to ask. And it recurs at the Electoral Commission, which can treat a conference-sponsorship fee from a BVI-controlled shell as a permissibility question, Part 8’s Zebec artery, but cannot ask the prior question of what the shell is for. Every agency answers the narrow question it is built to answer. None can ask the wide one. The structure survives in the gap between the questions.

The instrument that was captured, not evaded

There is a larger enforcement gap than any of the domestic ones, and the series has set it up since Part 1 without yet collecting on it. The dollar correspondent system is not only a payment network. It is the West’s principal instrument of statecraft short of war: the power to exclude a state from the means of international settlement, the measure imposed on Russia in 2022, on Iran over its nuclear programme, on North Korea over proliferation. The whole parallel substrate, the bill’s central exhibit, exists to route around that perimeter. The obvious reading is that the rails defeat sanctions by evasion, that USDT settling a Russian gold sale in Mali is simply value moving where the OFAC list cannot reach. That reading is true as far as it goes, and Part 7 documented it. But the deeper finding, visible only now that the holder class sits in the cabinet, is stranger and worse. The sanctions instrument is not being evaded. It is being privatised, exactly like the seigniorage and exactly like everything else in this series.

Watch the mechanism. In 2022, after the US action against Tornado Cash, Tether publicly declined to freeze sanctioned addresses pre-emptively. By 2025 the posture had reversed completely. In March 2025 Tether froze twenty-three million dollars tied to the sanctioned Russian exchange Garantex, in concert with the US Secret Service. In April 2026 it blacklisted two Tron wallets holding three hundred and forty-four million dollars of Iranian funds, under an OFAC campaign the Treasury named “Economic Fury,” and the freeze was announced not by a regulator but by Scott Bessent, the Treasury Secretary, personally, on his own account. Across the period Tether has frozen something over four billion dollars in total, more than two billion of it at the request of US agencies, across more than two thousand cases, and the GENIUS Act now requires every stablecoin issuer to build the freezing capability into the token itself. The act of state that is a sanctions freeze, the exclusion of a designated party from settlement, is now performed by pressing a button, and the button belongs to a private company in which the largest single shareholder funds a British political party and roughly five per cent is held by the family bank of the serving Commerce Secretary.

That is not the defeat of the sanctions instrument. It is its transfer into private hands aligned with one cabinet, and it is more dangerous than evasion would have been. A perimeter enforced by the public correspondent system was, for all its faults, a rule of the system: applied by states, reviewable, multilateral in the cases that mattered. A perimeter enforced by an issuer’s freeze function is a discretion, exercised by a private party, on the instruction of whichever principals it is aligned with. The same instrument that froze Iranian wallets to order is the instrument settling Russian-aligned gold through the African rails the bill has just itemised, and nothing in its structure compels it to treat the two alike. It freezes what it is asked to freeze by the people it answers to, and lets pass what they do not ask about. The Western enforcement power has not been bypassed. It has been bought, and handed to a cabinet that holds the equity. The strategic prize is not a world with no sanctions. It is a world where the power to sanction belongs to the holders of the trade, to be aimed at their enemies and withheld from their partners, which is the same regressive capture the rest of the bill describes, applied to the last instrument the West had left.

If the diagnosis is enterprise and the gap is that no agency can see enterprise, then the response, however uncomfortable, is an instrument that can. The Rycroft Review of March 2026 took the first half: a hundred-thousand-pound cap on overseas-resident donations, a ban on crypto donations, strengthened Electoral Commission powers and better inter-agency coordination. That closes the funding vector, and it is why both the Harborne megadonor artery and the Zebec shell artery were clamped in the same month. But the funding vector is half the problem. The other half is the structure that the funding vector feeds, and a donations cap does not reach a structure. Reaching it would require something this series has called, as shorthand, Operation Iron Veil: a standing cross-agency unit with police, intelligence and treasury inputs, and behind it an enterprise statute on the RICO model that does not require proof of a central conspiracy, only proof of a continuing enterprise engaged in a pattern of qualifying acts. The Electoral Commission cannot prosecute enterprise. RICO does not ask it to find a plot. It asks it to find a structure of named people in named relationships producing a pattern, and that structure is precisely what the public record already contains. The objection to such an instrument is real and serious: an enterprise statute aimed at political-financial structures is an enormous power to hand a state, and the history of broad racketeering statutes is a history of mission creep. That objection should be argued out in the open. But it should be argued against the actual alternative, which is not the status quo ante. It is a structure that the existing instruments have already demonstrated, in a week of dismissal letters, they cannot touch.

The bill, itemised

A bill should have numbers on it, so here are the ones the eight parts have earned, gathered in one place for the first time.

The yield leg. Tether alone booked over ten billion dollars of profit in 2025 and paid out more than ten billion in dividends in the first three quarters, on a reserve of roughly 141 billion dollars of US Treasury exposure backing around 186 billion of circulating USDT. That profit is, in substance, public seigniorage collected privately: interest on the dollar’s network value, earned on the way down. The sector collectively holds something over 182 billion dollars of US Treasuries, more than most sovereign states. The single largest owner of the single largest issuer is the single largest donor in British political history.

The donation leg. Christopher Harborne has directed more than 24 million pounds to Reform UK since 2019, roughly two-thirds of everything the party has ever raised, including a record nine-million-pound gift in August 2025, with a lifetime figure across his Conservative-era giving of around 30 million. Separately and undeclared, a five-million-pound personal gift to Nigel Farage in early 2024, now before the Parliamentary Commissioner. In the United States the crypto sector’s Fairshake committee deployed 45 million dollars in the 2024 cycle, Ripple added five million in XRP to the Trump inaugural, and the Winklevoss and Thiel and adjacent vehicles layered tens of millions more. The donations are not the trade. They are the customer-acquisition cost of the trade, and against ten billion a year of captured yield they are a rounding error, which is the entire point: a four-figure-return position protected by a single-figure-percentage outlay.

The compute leg. Stargate is a 500 billion dollar initiative; the anchor OpenAI contract is reported at over 300 billion; Ellison’s Oracle stake ran past 300 billion dollars in 2025 on the strength of it, about a third of it pledged against personal debt. The TikTok US restructuring put a fifteen-per-cent distribution stake in the same Oracle-led hands.

The gold leg. Central banks have bought more than a thousand tonnes a year since 2022. The American gold reserve is carried at 42.22 dollars an ounce against a market price more than sixty times higher, a latent revaluation gain on the order of three-quarters of a trillion dollars, and a February 2025 executive order exists to monetise it.

Total the legs and the headline is plain enough: eight to ten billion dollars a year of public yield privatised today, rising an order of magnitude on the float’s own forecasts, against standing positions in gold and compute measured in the high hundreds of billions. The legs are denominated in different things, annual profit, latent revaluation, market capitalisation, and the honest move is to keep them distinct rather than fuse them into one spurious figure. But distinct does not mean unaddable. The recurring extraction has a number, the standing positions have numbers, and the reckoning at the end of this part puts both beside the people who pay them. The bill is not unwritable. It has simply never been written down in one place.

Where the bet becomes territory

The four legs are financial, but two of them touch ground, and the ground is where the trade stops being an abstraction and starts being a war. A position is only a position until the thing it is a claim on has to be defended or seized, and the resource leg and the compute leg each rest on a specific piece of contested earth. Name them, because the series has circled both and never set them side by side.

The resource leg rests on Ukraine. On 30 April 2025 the United States and Ukraine signed the Reconstruction Investment Fund, a fund jointly and equally managed, capitalised by revenues from new Ukrainian mineral, oil and gas licences, giving American firms priority access to the titanium, lithium, graphite and rare-earth deposits Part 6 catalogued, and the signature voice on the American side was Scott Bessent, “economic security is national security,” the man whose monetary vocabulary Part 5 traced to Leesburg. Read in isolation it is a reconstruction agreement. Read against the bill it is the resource leg acquiring its mine, and the terms are the tell: Kyiv signed it hoping a commercial stake would buy the continued military support that no clause in it actually guarantees, which is to say the country was asked to trade its mineral future for the mere possibility of being defended. Two months earlier, in the Oval Office scene Part 8 closed on, the same President had told the same Ukrainian president he held no cards and should be more grateful, with Bessent in the room. The deal and the dressing-down are one event. A country fighting for survival is told the price of arms is the subsoil, and the man setting the price is the man selling the doctrine.

Except the cards have since changed hands, and that reversal is the single clearest refutation of the doctrine the series has found. The doctrine’s oldest assumption, the one spoken aloud in that Oval Office, is that Ukraine is a transient obstacle, a supplicant with nothing to offer, delaying a settlement history has already decided. By 2026 the assumption is simply false on the evidence, and the evidence is in Ukraine’s own hand. In a letter to the President and Congress dated Memorial Day, 26 May 2026, Volodymyr Zelensky set out the new ledger plainly: Ukraine had built a drone industry that, in his words, now outpaces Russia’s, had taken its interception rate against Russian and Iranian-designed attack drones past ninety per cent, and was offering that capability to allies through the Drone Deals format it had already proposed to the United States. Three years of the most intense drone and missile war Europe has seen since 1945 had turned the supplicant into a supplier, and the letter named the customers: when Jordan, Saudi Arabia, Qatar, the United Arab Emirates and Kuwait reached out, Ukraine sent specialists who strengthened air defence across the Gulf, including, in the detail that inverts the whole doctrine, the protection of American bases. The country told two years earlier that it held no cards now defends the patron’s installations in the patron’s own client states, and describes its army, not implausibly, as the largest in Europe and the only one tested by modern war.

The reversal is real but it is not total, and the same letter is honest about the limit, which is what makes it credible rather than triumphal. Ukraine leads the world in drones and has next to no capacity of its own in ballistic-missile defence; for that it still depends almost entirely on American Patriots, and the letter is in the end a plea for them, written because the supply is not keeping pace and batteries stand, in Zelensky’s phrase, with no missiles loaded. And here the Iranian gamble closes the loop with brutal economy, because the reason the interceptors are scarce is named in the letter itself: demand has spiked in other regions, “especially given the situation in the Gulf.” The munitions Ukraine needs to stop Russian ballistic missiles are the same munitions the Iran adventure is consuming. So the picture is exact and double: Ukraine is the arsenal of the drone war and the supplicant of the missile war, an exporter to the Gulf and a beggar for Patriots, and both halves are true at once. But even the partial reversal is fatal to the doctrine. The doctrine said Ukraine was the obstacle. The battlefield made it, at minimum, the indispensable arsenal of European defence, with the United States shopping in its showroom for drones while Ukraine queues at America’s for interceptors. The transient obstacle is now the going concern, and a settlement history had supposedly already written is being unwritten, in Kyiv, one drone contract at a time.

The compute leg rests on Taiwan. This is the dependency the bill has so far left implicit, and it is the largest single point of fragility in the whole structure. The Stargate buildout, the three-hundred-billion-dollar contract, Ellison’s three-hundred-billion-dollar stake, the entire compute brace, runs on advanced chips, and one company in one place makes them: TSMC manufactures over ninety per cent of the world’s most advanced semiconductors, and sends every one of them, even those fabbed at its new Arizona plant, back to Taiwan for the final packaging step that no one else can yet do at scale. The island that makes the chips is the island Beijing intends to absorb, and the markets that price the compute leg as a one-way bet on infinite AI demand are, in the analysts’ own word, “systematically underpricing” the chance that the supply is cut at source. The compute leg is therefore a leveraged position, Ellison’s a third pledged against debt, Musk’s the same pattern, written on the assumption that a contested island stays open. If gold is the asset that reprices when the dollar erodes, Taiwan is the asset that reprices, instantly and catastrophically, the day the strait closes. The whole optimistic side of the trade, the transcendent future Part 8’s retailers sell, is collateralised by a fab complex inside the range of Chinese artillery.

Put the two together and the alignment the series has tracked resolves into a single posture. The trade is long the erosion of the dollar order and short the Western alliance that secured it: it profits as the old settlement decays, on the gold side, on the yield side, on the sanction-capture side. So its political and doctrinal layers push, with remarkable consistency, exactly the positions that accelerate the erosion, abandon Ukraine, accommodate over Taiwan, treat both as obstacles to a settlement history has supposedly already decided. This is not because the retailers have studied a map. It is because a holder class hedged for the dollar’s decline has no stake in the alliances that would arrest it, and every stake in their dissolution. Ukraine and Taiwan are where that indifference becomes lethal: the two places where the financial bet is settled not in basis points but in territory and in lives, paid, as the rest of the bill is paid, by people who never saw the cap table.

The prize, and why it was always the prize

Part 7 introduced a strange document and left it half-explained on purpose, holding the payoff for here. Anton Vaino, the career official Vladimir Putin appointed chief of staff in August 2016, had published in 2012 a paper called “The Capitalization of the Future,” which the BBC’s Russian service surfaced when he rose to the post. In it Vaino described a device he named the nooscope: a sensor, in the cosmist tradition Part 7 set out, for recording the noosphere, the sphere of collective human thought and activity. Part 7 flagged the obvious objection, that this reads as mysticism, and then quoted the line that makes it something else. Vaino’s co-author Viktor Sarayev told the BBC plainly what the nooscope was for: it “scans transactions between people, things and money.” That is the sentence to hold in mind, because it is not mysticism at all. It is a description of a surveillance instrument whose object is the ledger of human activity itself, every exchange between every person, every object and every unit of money, recorded and made legible to whoever holds it. Part 7 presented this as the doctrine’s deepest layer, the thing underneath the geopolitics. Here it becomes the answer to the question the whole series has been circling: why payment infrastructure, of all things, is the prize.

Because read against everything the eight parts have documented, and in particular against the parallel payment substrate itemised above, that sentence stops being a curiosity and becomes a thesis statement from the other side. A system that scans every transaction between people, things and money is not a metaphor for a payment network. It is a payment network, described by one of its theorists. The doctrine that fuses surveillance of the payment rails with the cosmist promise to transcend scarcity and death is not having that fusion imposed on it by a hostile reading; its own architects wrote the fusion down, in a paper by a man who now runs the Russian presidential administration. So capturing the payment infrastructure is not a side effect of the trade, a convenient yield to be skimmed while the real prize lies elsewhere. In the doctrine’s own terms it is the prize. The rails are the noosphere made legible: own them and you own the record of every transaction between people, things and money, which is to say you own the capitalised future the paper is named for. This is why the substrate matters beyond the yield it throws off. The ten billion dollars of captured seigniorage is the trade’s revenue. The rails themselves, the ledger of who paid whom for what, are the asset, and the asset is the thing the doctrine has wanted all along. The Western mirror of this, the TESCREAL bundle Part 8 named, promises the same transcendence in optimistic dress. Musk retails it as a lifestyle. Thiel funds the canon that calls it wisdom and the Palantir layer that wires the same transaction-watching into the American security state. East and West, the deepest layer of the doctrine agrees on what is worth owning, and it is the rails, because the rails are where the watching happens.

The continent that is the laboratory

There is one more total to take, and it is the one the series has been most careful to build the evidence for and slowest to name, because naming it plainly is the part that the contaminated vocabulary works hardest to prevent. The privatisation does not fall evenly on the world. It has a primary site, and the site is Africa.

Assemble what the eight parts have placed there. The mobile-money rails that the substrate runs on, M-Pesa and MTN and Airtel and Orange, carry most of the world’s mobile-money users across the continent. JUMO, the banking-as-a-service layer for the unbanked, is Mauritius-registered, Gemcorp-financed, and sits behind a sitting member of the House of Lords through beneficial ownership he never declared. Its lending runs on a revealing division of labour: JUMO supplies the platform and the data, the mobile operators MTN and Airtel and Tigo supply the customers, and a bank supplies the balance sheet, funding the loans and holding the treasury while JUMO manages the wallet under the bank’s instruction. The bank, across much of the continent, is Absa, which is to say Barclays under a later name. And here Barclays earns a second look, because it keeps appearing. This is the institution two Quaker goldsmiths founded in Lombard Street in 1690, that financed merchants in the American and Caribbean colonies and whose Barclay partners were, by the 1750s, engaged in the slave trade, that built a branch network across British Africa in the twentieth century, that ran its City investment arm as Barclays de Zoete Wedd through the Big Bang decades, that rebranded its African franchise as Barclays Africa, then sold the controlling stake down from 2016 and left the network behind as Absa, locally listed, the name changed, the franchise intact. The same bank, under whichever name the era required, has been present at the British end of African resource extraction for three centuries, and it is present now, holding the balance sheet behind the rail that banks the unbanked. The arrangement is its own small allegory: the old empire’s bank holds the money, the new empire’s rail runs the accounts, and the customer, banked at last, transacts on infrastructure owned by neither of the two empires nor by herself. Swoop, the Thiel-Fellow venture, states the thesis without embarrassment: in Africa there is no legacy banking infrastructure, so you do not compete with the old rails, you build the new ones and own them, and that absence is named, in the funding deck, as the opportunity. Gemcorp’s capital is Russian in origin and African in destination, routed through London peerages that supply the letterhead. The gold leaves Mali and the Central African Republic and Sudan in convoys and settles outside the dollar, Part 7’s subject. The uranium offtake runs through Namibia, the bauxite through Guinea, the cobalt and the lithium and the rare earths through the Congo and the copperbelt, Part 6’s subject. Set these beside one another and the pattern is not a series of separate ventures. It is a single posture toward one continent: extract the resources, own the rails the payments run on, and conduct the monetary experiment, the stablecoin remittance corridor, the crypto settlement layer, the banking-the-unbanked pilot, on a population that has the least power to refuse it and the least recourse when it fails. Africa is not a market the trade happens to reach. Africa is the laboratory in which the trade is run before it is run anywhere else, and the test subjects did not consent to the trial.

Look at who is conducting it, because the composition is its own argument. A cluster of the principals are white men born in or made in southern Africa: Elon Musk, born in Pretoria; David Sacks, born in Cape Town; Peter Thiel, who spent part of his childhood in Swakopmund in what was then South West Africa, now Namibia, where his father managed work at the Rössing uranium mine; Lord St John of Bletso, whose entire commercial portfolio is African resources and African finance. Alongside them the American and European capital that funds the substrate, and alongside that the Chinese state, which is assembling through Barrick’s joint ventures and the Laroucheite Belt and Road infrastructure and the mineral offtakes something that is, in plain description, an African empire bought rather than conquered, and the Russian state, which settles its African gold and sells its African influence through the same rails.

A continent that spent the twentieth century expelling formal empire is, in the twenty-first, being re-divided, by some of the same bloodlines and some of the same capitals and two new ones in Beijing and Moscow, into spheres of resource and monetary control. The mechanism is no longer the gunboat and the charter company. It is the cap table, the offshore vehicle and the payment rail. But the structure, a foreign-owned extractive apparatus operating a captive population’s economy for the benefit of distant shareholders, is the structure the word colonialism was coined to describe.

And here is the part that makes it durable, the part that is the whole reason this series needed a proper methodology and structure. The project is defended from both ends of the political spectrum at once, by people who believe they are opposing it. The anti-imperialist left looks at a system being built to bypass the dollar and the Western banking perimeter and sees a liberation: the Global South escaping the clearing system that has disciplined it for fifty years, the decolonisation of finance, a multipolar future. The libertarian right looks at the same system and sees a different liberation: private money escaping the central banks, the unbanked granted access at last, the dead hand of the state lifted off the individual’s wallet. Both are cheering. Both believe they are striking a blow against power. And both are supplying the political cover for a project whose actual beneficiaries are a stablecoin issuer booking ten billion dollars of the public’s yield, a Chinese state buying a continent’s minerals, a Russian state laundering its gold, and a handful of men with southern-African childhoods who have worked out that a population with no legacy banking infrastructure is a population whose entire financial life can be built, from scratch, on rails they own. The left calls it anti-imperialism. The right calls it freedom. It is the most efficient imperialism ever designed, because it has persuaded its victims’ would-be defenders to argue its case. That is what the contaminated vocabulary is for. It is the language in which a colonisation gets itself described as a liberation by the very people who would oppose a colonisation, and it works because each side is only ever shown the half of the project that flatters its priors. Show the left the bypassed dollar and hide the Mauritius beneficial owner. Show the right the banked unbanked and hide the Chinese offtake. Nobody is shown the whole, and the whole is the point.

The two settlements

Bretton Woods, in July 1944, was a public settlement. Forty-four states met in New Hampshire and built a monetary architecture, fixed rates, a gold-pegged dollar, the Fund and the Bank, to underwrite a security architecture, of which NATO would be the military leg. Both were run by states, in the open, for stated public purposes, and when the first leg failed it failed in public too: a unilateral American default announced on a Sunday evening in fifteen minutes of television, an event with a date and a clock time. The settlement was a thing states did to each other, and you could watch it happen.

The New Bretton Woods, in 2026, is a private settlement. The same monetary architecture is being asset-stripped, the dollar’s reserve yield privatised on the way down and its replacement metal pre-positioned for the way up, while the security architecture that underwrote it is either captured, through cabinet positions held by people whose vocabulary traces to a mail-fraud convict’s economic desk, or dismantled in real time, through the abandonment of an ally in an Oval Office and the erosion of foreign-influence enforcement. And it is not happening as an event. It has no Sunday, no clock time, no fifteen minutes of television. It is happening as a method: in nine-figure donations and cap-table lines, in a BVI shell sponsoring a rule-of-law panel, in a stablecoin prospectus and a sovereign-wealth executive order, in a dismissal letter and a dinner in Brussels and a podium in Moscow shared by two men selling the same future. The first settlement ended on a Sunday at nine in the evening. The second is not going to end on any particular day, because it was never designed to end. It was designed to accrue.

So total it. The series promised a bill, and a bill has a number on it, so here is the number, with the working shown.

Start with the part that recurs every year and is already audited. The stablecoin sector holds something over 182 billion dollars in US Treasuries. At a yield of roughly four and a half per cent, that float throws off on the order of eight billion dollars a year, and Tether’s own disclosure confirms the scale from the other direction: over ten billion dollars of profit in 2025, more than ten billion paid out in dividends in nine months. Call it eight to ten billion dollars a year, today, of interest that until stablecoins existed accrued to the US Treasury and through it to the public, now booked as private profit. That is not a projection. It is the current run-rate, and it compounds. On the sector’s own growth forecasts, a float approaching two trillion dollars by the end of the decade, the same yield produces something near ninety billion dollars a year of privatised seigniorage. Set beside it the one-off positioning gains the series has documented: a latent revaluation of roughly three-quarters of a trillion dollars sitting in the gap between the book and market price of the American gold reserve, the asset a sovereign-wealth executive order exists to monetise; and several hundred billion dollars of paper wealth created on the compute leg, a third of it pledged as collateral. The recurring number is eight to ten billion a year and rising. The standing positions are measured in the high hundreds of billions. These are not estimates pulled from the air. They are the issuers’ own attestations, the Treasury’s own statutory valuation, and the market’s own pricing, added together for the first time.

Now the question the series has been building toward and the official literature never asks: who pays it? Seigniorage does not evaporate when it is privatised; it is transferred, and a transfer has a payer at each end. At one end stands the dollar-system taxpayer. Every dollar of yield a stablecoin issuer keeps is a dollar the Treasury must raise instead by borrowing, and service, and the servicing falls on the public balance sheets of the United States, Britain and the rest of the dollar world. At the other end stands the stablecoin holder, and the series has already shown who that is: disproportionately the resident of the inflation-stricken, capital-controlled, under-banked economy, the Argentine protecting savings from the peso, the Nigerian moving money the formal banks will not move, the African on the JUMO rail. The float is built from the dollars of the world’s least powerful, and the yield on those dollars is collected by the world’s most powerful, and the gap in between is the trade. The bill is paid twice, at both ends, by the people at each end with the least power to refuse, and it is collected in the middle by a holder class whose largest single figure funds a British political party and whose custodian sits in an American cabinet. That is the incidence of the privatisation, stated plainly: a regressive transfer of the dollar’s public yield, upward and inward, from the global poor and the general taxpayer to a few hundred named people, running now at the better part of ten billion dollars a year and engineered to grow.

That is the bill. Eight to ten billion dollars a year of public seigniorage, today, converted to private profit, rising toward ten times that within the decade, against standing positions in gold and compute measured in the high hundreds of billions, paid for by the dollar-system taxpayer and the unbanked saver at once, and protected by political agents who now sit in the cabinets meant to guard the thing being taken. And alongside the money, the instrument: the power to sanction, the West’s last lever short of war, lifted out of the public correspondent system and rebuilt as a private freeze function aligned with one cabinet, to be aimed at enemies and withheld from partners. The strategic beneficiaries are the holder class and the states buying the gold by the thousand tonnes. The strategic losers are the public balance sheets of Britain, the United States and Europe, the African populations on whom the apparatus is field-tested, and Ukraine and Taiwan, the two countries whose ground is the collateral on the resource and compute legs and whose defence the trade is positioned to see abandoned. None of it is secret. All of it is disclosed, in prospectuses and attestations and registers and a sovereign-wealth order. It has simply never been added up, because adding it up requires reading the donations, the cabinet posts, the offshore owners and the dinner seating as a single document, and the people in that document have arranged, by spreading it across nine figures and three jurisdictions and fifty years, that nobody ever does. This series added it up. The number is real, the payers are named, and the ledger is left open because the trade has not closed.

The house always wins

There is a final reckoning, and it is the one that turns the whole series from an account of a scheme into an account of a truth, because it asks the only question that ultimately matters: after all of it, who actually won?

Start with the states, because they did the planning. Russia spent a quarter of a century and a generation of men on the restoration of an empire, and has a smaller one than it began with: NATO larger by two members, the army ground down at an airport outside Kyiv, the leader physically isolated and reduced to threatening weapons he cannot use to end a war he cannot win, and, in April 2026, his last reliable friend inside the European Union voted out of office in Budapest on a wave of leaked recordings of exactly the Moscow intimacy the series has documented, the Orbán-Putin and Szijjártó-Lavrov calls surfacing days before the ballot and turning it. China spent two decades and a continent’s worth of credit on a Han restoration that was to include Taiwan, and holds an economy in a four-and-a-half-year property collapse, gross debt near three hundred per cent of output, the lowest growth target in its modern record, a deflationary spiral its own economists call a trap, ghost cities standing empty, and a semiconductor industry that pours state money into fabs it cannot yet bring to the leading-edge node, which is to say it cannot make at scale the one component the entire future it is buying depends upon. Iran spent forty years and a fortune building a Shia arc from Tehran to the Mediterranean, and watched the proxies degraded, the air defences breached, the wallets frozen to order, the arc broken. Three empires planned for. Three empires not built. The cosmist promise of Part 7, the resurrection, the noosphere, the capitalised future, has delivered to its believers a smaller Russia, a poorer China and a weaker Iran. And the country all three, and the doctrine’s own retailers, agreed to write off, Ukraine, the supplicant with no cards, has emerged from the wreckage as the arsenal the rest of them now queue to buy from, its drone specialists deployed across the Gulf defending, among other things, American bases.

Now the retailers, because they did the selling. Trump’s coalition is fracturing under the weight of an Iran adventure it never wanted and a cost of living it cannot fix. By late May 2026 his net approval sits at roughly minus twenty, around thirty-seven per cent approving against sixty disapproving, which is lower than Biden at the same point and lower than Trump’s own first term; his rating on prices, the issue voters rank first, has fallen in every single month of the year to minus forty-seven. The generic ballot for the November midterms runs four to eight points to the Democrats, who need only three seats to take the House, and the administration’s answer is not persuasion but a mid-decade redistricting scramble to carve the map before the vote, which is the move of an incumbency that has read the same polls and does not expect to win the argument. Abroad the alliance the doctrine was meant to peel apart is instead congealing: the United Kingdom and the European Union are closer in 2026 than at any point since the referendum, and Orbán, the model illiberal, the one reliable Moscow-aligned vote inside the Union, is simply gone. The political layer that was supposed to deliver the protected future is, on the present evidence, losing the elections it stands in and trying to redraw the boundaries of the ones it has not yet lost.

And the British retailer fares no better, which is the neatest illustration of all, because his troubles come from inside the trade. Nigel Farage was brought back to the front line of politics in 2024 on the largest donor fortune in the country’s history, and the same prominence now exposes every transaction he makes to a scrutiny he cannot switch off. The undeclared five-million-pound personal gift from Christopher Harborne, Part 8’s sharp object, sits before the Parliamentary Commissioner, and the procedural tail of that inquiry is the genuinely dangerous one: a suspension of ten sitting days would open a recall petition in Clacton, and a recall petition is a referendum on a politician at his least popular, which is a thing no amount of donor money can simply buy off. Money put him on the stage; the disclosure regime that money triggered now follows him across it. And his flank is being turned by the trade’s own techno-utopian financier. Elon Musk, who once bankrolled and boosted Reform, withdrew his support and in 2026 publicly endorsed Rupert Lowe’s Restore Britain, the breakaway to Reform’s right, which has surged to seven to ten per cent in national polling and threatens to split the anti-Labour vote in the very by-elections Reform needs to win. This is the no-central-coordination thesis of the whole series playing out in miniature, live: the financier and the retailer were never a partnership, only two positions that happened to align, and the moment they diverged the financier simply funded the competitor. Farage is being undercut not by the left, nor by the establishment he runs against, but by the same Musk complex Part 8 placed in the trade beside him. The retail layer is cannibalising itself, exactly as a set of self-interested positions with no conductor eventually must.

So run the scoreboard, and the pattern is total. Every actor with a territorial or national goal has failed to reach it. The Russian empire does not exist. The Han Taiwan does not exist. The Persian arc is broken. The MAGA settlement is cracking, its figurehead twenty points underwater and its party redrawing district lines because it cannot move voters. Decades of doctrine, manoeuvre, war and expenditure, and not one of the grand designs stands. And yet the bill this part has totalled is being paid in full, every year, on time. The eight to ten billion dollars of privatised yield does not depend on Russia winning, because it is collected whether the dollar is strong or weak. The gold position does not depend on China rising, because the metal reprices on fear alone. The compute fortune does not depend on the future arriving, only on the story about it holding long enough to borrow against. The trade was never aligned with any of the states it travelled alongside. It was orthogonal to all of them, and that orthogonality is the whole secret of it.

The money men did not need Russia to win, or China, or Iran, or even Trump. They needed only motion, instability, the erosion of the old settlement, the fear that drives the gold bid and the capital flight that fills the stablecoin float and the deregulation that frees the position. Their counterparties fought over territory and lost. They held the position and won, because the position was a claim on the volatility itself.

That is the deepest finding of the series, and it is older than any of the doctrines in it. In a casino, the gambler may believe in systems, in destiny, in the turn of the next card, and the gambler may be Russian or Chinese or Iranian or American, may dream of empire or restoration or transcendence. The house believes in none of it. The house does not bet on red or black. The house owns the table, takes a percentage of every wager, and is indifferent to which gambler walks away happy tonight, because the rake is collected on the playing, not the winning. Putin and Xi and the rest are the gamblers, and they are losing, as gamblers do. The men in the 2017 photograph, the holders of the stablecoin float and the gold and the compute and the rails, are the house. They funded the table, they take the rake, and they have arranged, through the donations and the cabinet seats and the offshore vehicles this series has spent nine parts tracing, that whoever else loses, they are paid. The strategic contest the contaminated vocabulary frames as a battle between a declining West and a rising East is, read against the cap table, a battle between gamblers who will all eventually lose and a house that has already won. That is the bill, finally understood. It is not the cost of one side’s victory. It is the rake or commission taken on everyone’s defeat.

Back to Part 1, on the public settlement of 1944 and the Sunday it ended; Part 3, on how stablecoin float became a private claim on Treasury yield; Part 6, on gold as the second leg of the single trade; and Part 8, on the retailers who sell the politics that protects it. The series ends here, with the invoice presented and the ledger left open, because the trade it describes has not closed.

A website will be launched shortly to show this series in more detail with further evidence and an interactive map.

I’m absolutely blown away. Enterprise 🤯. It’s like they are using the separation of powers we built to protect things to steal it ALL. And each billionaire knows their role.

Indeed impressive!

Thanks Matt!

Also looking forward to the website!